FAQ on Carbon Footprints and Climate Neutrality

Process – Context – Balancing – Verification – Communication

Context

Climate change is caused by the greenhouse effect: Greenhouse gases in the Earth's atmosphere allow solar heat to enter the atmosphere, but hinder its radiation back into space. Many of these gases are natural components of the Earth's atmosphere. However, human activity has greatly increased the concentration of some greenhouse gases. CO2 is the greenhouse gas that is produced most by human activities in terms of quantity: 63 % of the global warming caused by humans is attributed to it.

The CO2 concentration in the atmosphere is 40 % higher today than at the beginning of industrialisation. Other greenhouse gases are also emitted in smaller quantities, but they hinder the radiation of solar heat back into the universe thousands of times more effectively than CO2. 19 % of man-made global warming is due to the greenhouse gas methane (CH4), 6 % to nitrous oxide (N2O). Fluorinated gases account for most of the rest. The amount of greenhouse gases naturally occurring in the atmosphere is increasing enormously, mainly due to the use of fossil fuels, deforestation of rainforests and livestock farming.

[05.05.2026]

Rising average temperatures and steadily rising sea levels are just two of the many impacts of climate change. It leads to a change in climate variability – strong short-term climate fluctuations and more frequent extreme weather events such as heavy rain or hot summers are the results.

Particularly threatening risks are the reduced quality and quantity of drinking water and growing conditions for staple foods. The changed or prolonged occurrence of biological allergens (e.g. pollen) and the increased occurrence of so-called vectors (disease carriers such as ticks or mosquitoes) are also a cause for concern. The shift in the periods in which plants grow, flower and bear fruit also has an impact on agricultural production.

The economy and transportation are also affected: Roads and railways are washed out by heavy rainfall and suffer from high temperatures, inland waterways are affected by high or low water. In addition, many power plants draw their cooling water from rivers and feed it back in after it has been heated: If the river water is too warm or severely depleted by the summer heat, power plants have to be shut down in an emergency.

[05.05.2026]

CO2 neutrality is the state of equilibrium between the emission of carbon dioxide and its absorption from the atmosphere in so-called carbon sinks.

Greenhouse gas neutrality considers all other greenhouse gases in addition to CO2. This means that greenhouse gas neutrality is achieved when no greenhouse gases are emitted over and above those that can be absorbed by nature or other sinks.

However, in addition to greenhouse gases, other indicators also play a role in global warming, such as the contamination of soil and water, the consumption of raw materials and the loss of biodiversity. Accordingly, climate neutrality is only achieved when all of these effects on the climate have been neutralized. Including all environmental impacts is essential in the fight against climate change, but it is very complex and practically impossible for organizations to do.

In line with the United Nations Framework Convention on Climate Change, the focus is therefore initially on achieving greenhouse gas neutrality. The ISO 14068-1:2023-11 standard published at the end of 2023 calls this state, in which all unavoidable emissions are offset, i.e. when GHG emissions and GHG removals are in balance, "carbon neutral". As the standard has not yet been translated into German, we also call it "carbon neutral" in the meantime.

[05.05.2026]

When drawing up greenhouse gas balances (carbon footprints), as the name suggests, not only carbon dioxide but also other climate-effective greenhouse gases are considered. These climate-relevant gases were defined in the Kyoto Protocol and assessed annually by the Intergovernmental Panel on Climate Change (IPCC).

In addition to CO2, gases such as methane (CH4), which is mainly released by agriculture and gas leaks, are also included in the balance. They also include various coolants, nitrous oxide (N2O) from fertilizers and the chemical industry as well as sulphur hexafluoride (SF6), which is used as an insulating gas in high-voltage technology.

All of these additional gases have a much greater impact on the climate than CO2. In order to be able to compare the relevance of the gases more clearly, the so-called "Global Warming Potential" (GWP) was defined.

The GWP of methane, based on the effect over 100 years, is 28. This means that the effect on the climate of 1 t of methane is just as damaging as that of 28 t of CO2. Partially halogenated or perfluorinated hydrocarbons in particular often have four-digit GWP values. The scale goes up to SF6 with a GWP of 23,500.

In order to be able to present carbon footprints in a comparable way, the total amount of greenhouse gas emissions is therefore also stated in so-called CO2 equivalents (CO2e) in addition to the breakdown into individual gases. Here, non-CO2 greenhouse gases are converted into CO2e via their GWP.

An example illustrates this:

If a company had an annual emission volume of 100 t CO2 and 1 t CH4, the company's carbon footprint would be 128 t CO2e.

[05.05.2026]

Responsibility for environmental protection affects all industries. However, emission-intensive sectors such as energy production or heavy industry (steel, aluminium, etc.), for which concrete measures have already been defined in the climate package, have a special role to play. The focus is also on companies whose products are supplied directly to end consumers (B2C), such as food or car manufacturers and the public sector. The food industry and the trade in particular can no longer ignore the issue of greenhouse gas accounting and carbon neutrality.

In the B2B sector, carbon neutrality is playing an increasingly important role in the awarding of contracts; in the B2C sector, it can influence public image, sales figures and thus market share.

[05.05.2026]

The carbon footprint is expressed in tonnes of CO2e. But how can you imagine a tonne of CO2? Here are a few examples:

- drive 9500 km with one car

- heat an average flat for 2 months

- a flight for one person from Brussels to Marrakech (~ 2350 km)

- the amount of CO2 that a beech tree binds in about 80 years of growth

- the volume of a cube made of one gaseous tonne of CO2 would have an edge length of eight meters under normal conditions.

[05.05.2026]

Balancing

Greenhouse gas sources are divided into three so-called "scopes" according to the Greenhouse Gas Protocol (GHG Protocol). The scopes are used in the greenhouse gas balancing of companies (corporate carbon footprints). When balancing products, the life cycle stages are considered.

Scope 1 includes all greenhouse gas emissions that occur directly within the company, i.e. emissions from the combustion of stationary sources (e.g. boilers), emissions from the combustion of mobile sources, e.g. from the company's own vehicle fleet, emissions from the company's production processes and fugitive emissions (especially coolants).

Scope 2 includes indirect emissions caused by the purchase of energy. This means that all emissions that occur when an energy supplier provides a company with electricity, natural gas or district heating, for example, are calculated here.

Scope 3 includes the remaining emissions from upstream and downstream supply chains that are related to the company's activities. This includes, for example, emissions from purchased goods and services, waste treatment, business travel, commuting and the product use. If the company produces petrol or diesel, for example, the emissions that are ultimately generated by the customer's use of these fuels are calculated here. The Greenhouse Gas Protocol divides Scope 3 emissions into 15 categories.

[05.05.2026]

According to ISO 14064-1, the organisation must report the quantities of direct greenhouse gases (GHG) by type of gas separately in tonnes of CO2e (CO2 equivalents). Relevant gases are CO2 (carbon dioxide), CH4 (methane), N2O (nitrous oxide), NF3 (nitrogen trifluoride), SF6 (sulphur hexafluoride) and other appropriate GHG groups such as HFCs (hydrofluorocarbons), PFCs (perfluorocarbons), etc.

According to the Greenhouse Gas Protocol, all greenhouse gases required by the UNFCCC/Kyoto Protocol at the time the company or product inventory is created must be included in the balance sheet, regardless of the standard. This currently applies to: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), sulphur hexafluoride (SF6) and nitrogen trifluoride (NF3). Other greenhouse gases can be specified as an option, but these must then be shown outside the balance sheet.

The CO2e indicates the greenhouse gas potential, i.e. the factor by which a greenhouse gas contributes to global warming compared to the same mass of CO2.

Emission factors that are used to calculate the carbon footprint are available without and, in the best case, with "upstream chains". With upstream chains means that they include emissions from upstream and downstream processes. For example, the emission factor for diesel without upstream chain only includes the direct emissions from the combustion of the fuel. The emission factor with upstream chain additionally includes emissions that occur during the extraction of the raw material, refining and through supply.

[05.05.2026]

Refrigerants are released through so-called leaks and, even in small quantities, can make a significant contribution to global warming.

[17.06.2026]

Scope 3 emissions are a consequence of the company's activities along the value chain. However, they arise from sources that are not owned or controlled by the company. In the GHG-Protocol, these activities are divided into upstream and downstream processes and comprise 15 categories.

Upstream:

- Goods and services purchased

- Capital goods

- Fuel and energy-related activities (not Scope 1 or 2)

- Upstream transportation and distribution

- Waste generated during operation/process

- Business travels

- Employee commuting

- Upstream leased assets

Downstream:

- Downstream transportation and distribution

- Processing of the products sold

- Use of the products sold

- End-of-life treatment of products sold (disposal/recycling)

- Downstream leased assets

- Franchises

- Investments

The determination of direct emissions is mandatory in accordance with ISO 14064-1 and the GHG Protocol. Indirect emissions must be assessed in accordance with ISO 14064-1 and considered in terms of their materiality. It should be noted that the materiality analysis must not be used to exclude relevant emissions from the balance sheet. According to the GHG Protocol only Scope 3 emissions are optional.

[05.05.2026]

When selecting emission factors (EF), a hierarchical prioritization should be followed. If possible, primary data from own measurements should always be used. If measurement is not possible, EFs from reputable databases can be used. If no corresponding EFs can be found in the databases, literature values can be used. If no suitable values can be found here either, plausible estimates may be used for the calculation:

Here is a list of reputable databases (excerpt):

- GEMIS (free, values for energy, material and transport systems)

- ecoinvent (fee-based, one of the best-known services)

- ProBas (free, with life cycle data, from UBA and Öko-Institut)

- EFDB (fee-based, English, contains emission factors of the Intergovernmental Panel on Climate Change (IPCC))

- Emission Factor Database (free, English, from various sources)

- Greenhouse Gas Protocol (free of charge)

- DBEIS (ex-DEFRA; free, English, some data UK-specific).

When selecting EF from databases, attention must always be paid to which life stages are included in the calculation of the EF. A distinction is usually made between EF including and excluding the upstream chain.

[05.05.2026]

If calculating your carbon footprint yourself is not an option for you, there are various calculation tools that can help you:

[05.05.2026]

Greenhouse gas emissions can be calculated according to the location-based and market-based approach for balancing the purchased electrical energy.

1. market-based method:

In this approach, the emissions from the electricity producers from whom the reporting party purchases electricity under contract are taken into account. This also includes electricity characteristics from contracted resources, such as guarantees of origin, purchased by the generator or the reporter itself.

2. location-based method:

This approach describes the amount of emissions that best reflects the emissions of the regional grid and corresponding electricity producers. For companies in Germany, we recommend using the values from the Federal Environment Agency.

When accounting for greenhouse gas emissions from companies, if market-based emission factors are available, values must always be calculated using both approaches and documented separately. For the accounting of product-related footprints, the market-based approach must primarily be selected; if these are not available, emission factors according to the location-based approach can be selected. The same requirements apply to the accounting of other Scope 2 categories such as steam procurement, district heating, district cooling and other energy sources.

[05.05.2026]

An emission factor for electricity is intended to reflect the emissions caused by electricity consumption. The balanced emissions of the electricity consumed are not necessarily the same as those generated during production. According to § 42 EnWG, every electricity supplier has a so-called electricity labelling obligation. According to this, the environmental impact must also be shown in g CO2/kWh. This corresponds to the market-based approach. The "residual mix" adjusts the production mix in such a way that the emissions of imported and exported electricity quantities are included in the balance and thus the guarantees of origin are taken into account. Further information on the residual mix can be found at the Association of Issuing Bodies (AIB).

[05.05.2026]

In order to correctly account for emissions from leased assets, it is first necessary to define the organization's consolidation approach and assign the type of lease. Leasing can be divided into two categories.

1. finance/capital leases:

This type of lease transfers all the risks and rewards associated with ownership of the asset to the lessee. Assets leased under a finance lease are considered wholly owned in the financial accounting and are reported as such in the balance sheet.

2. operating lease:

This type of lease allows the lessee to operate an asset, such as a building or a vehicle. However, none of the risks or rewards incidental to ownership of the asset are transferred to the lessee. Any lease that is not a financial or capital lease is an operating lease. An example here is vehicles in particular.

Depending on the consolidation approach, the emissions must then be allocated to Scope 1, 2 or 3. This results in four cases:

A. Consolidation approach "financial control or equity share approach and financial leasing":

In this case, the leased assets are treated as own capital assets. Direct emissions from operations are accounted for in Scope 1, energy-related emissions in Scope 2.

B. Consolidation approach "financial control or equity share approach and operating leasing":

There is no financial control or ownership of the leased asset. Direct and energy-related indirect emissions from operations must be accounted for in full in Scope 3.

C. Consolidation approach "operational control and financial leasing":

As leased goods are to be treated as own capital goods in the case of financial leasing and thus fall under operational control, direct emissions from operations are accounted for

in Scope 1 and energy-related emissions in Scope 2.

D. Consolidation approach "operational control and operational leasing":

The lessee has operational control over the asset, therefore direct emissions from operations fall under Scope 1, energy-related emissions in Scope 2.

To the original source of the response

[05.05.2026]

Offsetting certificates are not permitted in the context of either a corporate carbon footprint or a product carbon footprint, regardless of the underlying standard.

In contrast, ISO 14068-1 provides for offsetting through certificates from climate protection projects to achieve carbon neutrality. According to this standard, unabated and residual emissions must be offset by certificates.

Reliable offsetting has become a serious issue following reports of fraud and abuse in relation to carbon offsetting. It is therefore crucial to ensure that offsetting actually delivers the desired environmental benefits. The use of low-quality offsetting certificates can also have a significant impact on reputation (greenwashing). Various standards have been developed to assess the quality of offsetting. There is a detailed guide (in German) on this topic on the website of the Federal Environment Agency.

[05.05.2026]

Unabated greenhouse gas emissions: have not yet been reduced through suitable reduction measures as part of the Carbon Neutrality Management Plan.

Residual greenhouse gas emissions: remain after all technologically and economically feasible measures have been implemented.

Due to technological developments and changes in economic conditions, emissions that are still assessed as "residual emissions" today will be considered "unabated emissions" in the future.

[18.06.2026]

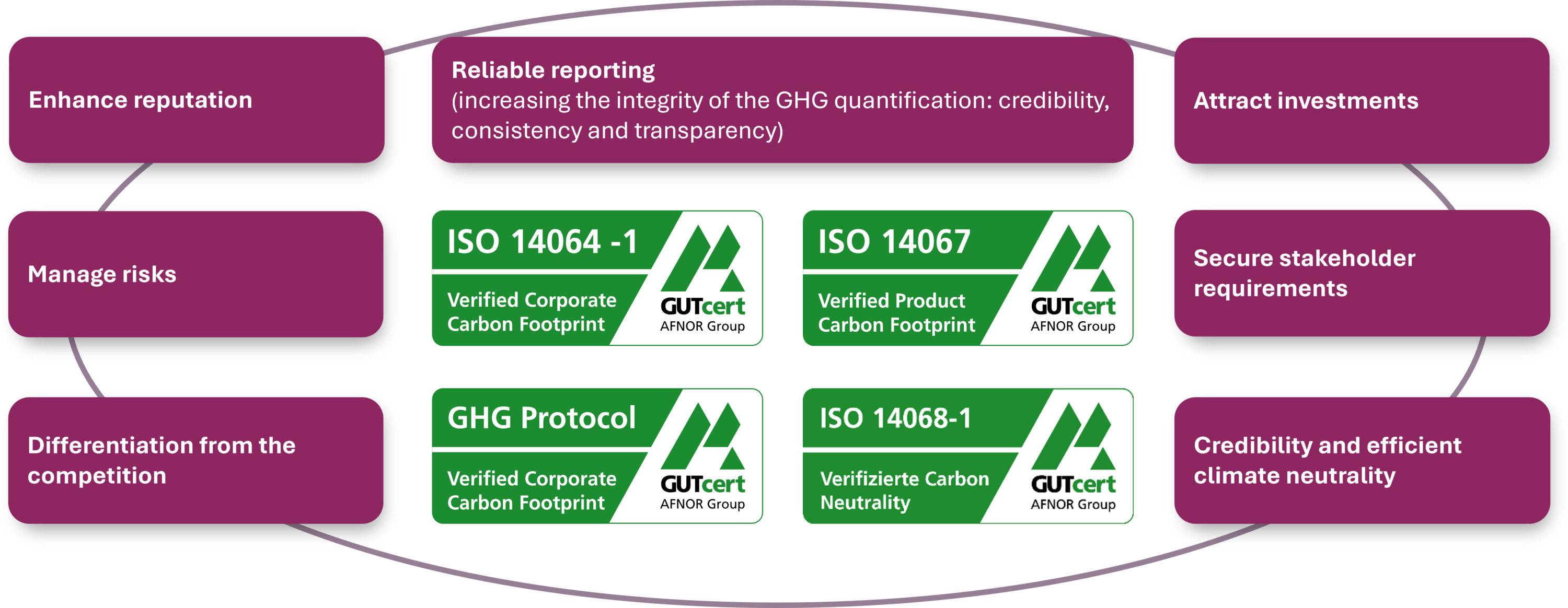

Verification

Corporate Carbon Footprint

- DIN EN ISO 14064-1: Specification with guidance at the organization level for quantification and reporting of greenhouse gas emissions and removals

- Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard

Product Carbon Footprint

- ISO 14067: Carbon footprint of products - Requirements and guidelines for quantification

- Greenhouse Gas Protocol: Product Life Cycle Accounting and Reporting Standard

Project Footprint

ISO 14064-2: Specification with guidance at the project level for quantification, monitoring and reporting of greenhouse gas emission reductions or removal enhancements

Climate neutrality

ISO 14068-1 was published at the end of 2023. GUTcert offers this audit to certify your carbon neutrality.

[05.05.2026]

The standards that can currently be verified are internationally recognized standard protocols according to which a carbon footprint or a climate neutrality strategy can be developed. Once your organization has been verified according to an appropriate standard, it is clear and open for everyone to see how and according to which criteria your carbon footprint or climate strategy was created. Findings from the carbon footprint can be communicated transparently and easily to the outside world.

[05.05.2026]

Since the end of 2023, products or entire organizations can be verified as carbon neutral on the basis of ISO 14068-1. In addition to a declaration of commitment from the management level, the first step is to determine the scope of the audit and its balance limits.

In the next step, you draw up the greenhouse gas balance in accordance with ISO 14064-1 or ISO 14067, depending on the area of application. However, other standards such as those of the Greenhouse Gas Protocol can also be used, provided they are consistent with the ISO standards.

The next step is to create and implement a carbon neutrality management plan in which you set out targets and measures for reducing and offsetting greenhouse gases. The specified hierarchy must always be observed: Reduction of emissions, removal of emissions within the balance sheet limits, offsetting - this is not an option, but an obligation. Only when all reasonable measures to reduce and remove emissions have been exhausted can the remaining emissions be offset with compensation certificates.

Finally, a Carbon Neutrality Report must be made publicly available for each reporting period, containing information on reduction, removal within the balance sheet limits and offsetting. The carbon neutrality claim may only be used once all of the aforementioned requirements have been met.

[05.05.2026]

The offsetting of emissions through the purchase and retirement of certificates is provided for by ISO 14068-1 and is required until the final phase of the reduction pathway. To ensure integrity, the standard places high demands on the certificates.

a) Certificates must be issued for actual reduction or increased removal of emissions

b) The additionality of the savings from the GHG project must be demonstrated by a robust assessment and go beyond legal requirements

c) Savings must be measurable in accordance with recognized methodologies for calculating emission credits

d) The permanence of the savings must be ensured. Appropriate safeguards should minimize the risk of reversal and ensure that, in the event of reversal, a mechanism is in place to guarantee that an equivalent reduction is delivered

e) The offset certificates must be certified by an independent body

f) The vintage of the certificates used may not be older than five years at the start of the carbon neutrality reporting period. In addition, the certificates used must be retired no later than 12 months after the reporting period.

g) Double counting of saved emissions must be ruled out. This applies to double counting by two organizations, but also by one organization and one national government. The latter can be ensured by so-called "corresponding adjustments" (Paris Agreement: 2015, Article 6, paragraph 4).

[05.05.2026]

Communication

A carbon footprint serves as a management tool for the implementation of CO2 and cost reduction plans and for the development of a clear climate strategy. The carbon footprint thus forms the basis for a company to make a contribution to mitigating the climate crisis.

External verification of the GHG balance safeguards your reporting, improves your reputation and serves as proof of the credibility of your climate neutrality.

[05.05.2026]

The current primary objective of Carbon Footprints is to identify potential savings. In addition, it should enable your organisation to develop a reduction plan and to document and communicate the reduction progress according to international standards.

Optionally, or when developing a climate neutrality strategy, emissions can be offset accordingly.

Comparisons between products is discouraged according to the current status of standards. The regulations on data collection allow the use of primary and secondary data, depending on whether direct emissions measurement is technically feasible and appropriate in terms of price. Due to the different data basis, there can therefore be considerable deviations when creating a carbon footprint for one and the same reference unit, depending on the collection method.

Especially in the case of greenhouse gas balancing of products, we currently strongly advise against comparative communication of the results. The product carbon footprint standard ISO 14067 sets clear and strict requirements for comparative statements (ISO 14025 as the basis for environmental product declarations). If it cannot be ensured that exactly the same balance limits and data basis have been used, no comparative communication may be made.

[05.05.2026]

A carbon handprint calculates the positive greenhouse gas impact achieved through an active improvement compared to a certain baseline value. This can be achieved, for example, by improving a customer's performance.

The concept can be used for marketing and communication purposes – you can communicate about your latest improvement or highlight the climate benefits of your products and services.

[05.05.2026]