Concrete reduction targets and effective measures can be derived from the systematically determined emission sources and continuously improved: you receive reliable data for your communication – with your stakeholders and the public.

Standards define principles and requirements for quantifying and reporting GHG emissions and sinks. This includes the development, reporting and verification of an organisation's GHG inventory.

To account for your company's greenhouse gases, you can choose between two established standards:

ISO 14064-1: Greenhouse gases – Part 1: Specification with guidance at the organization level for quantification and reporting of greenhouse gas emissions and removals

External verification ensures that your corporate carbon footprint is accurately calculated – your data is reliable at all times.

Credibility

Your verified greenhouse gas balance sheet clearly shows that transparent communication is important to you and that you take climate protection seriously.

Potential for Improvement

A detailed review of the completeness and methodology of data collection provides you with a sound basis for reducing your emissions in the long term.

Competitive Advantage

Your verified CCF is a competitive advantage for contracts that require emissions reporting.

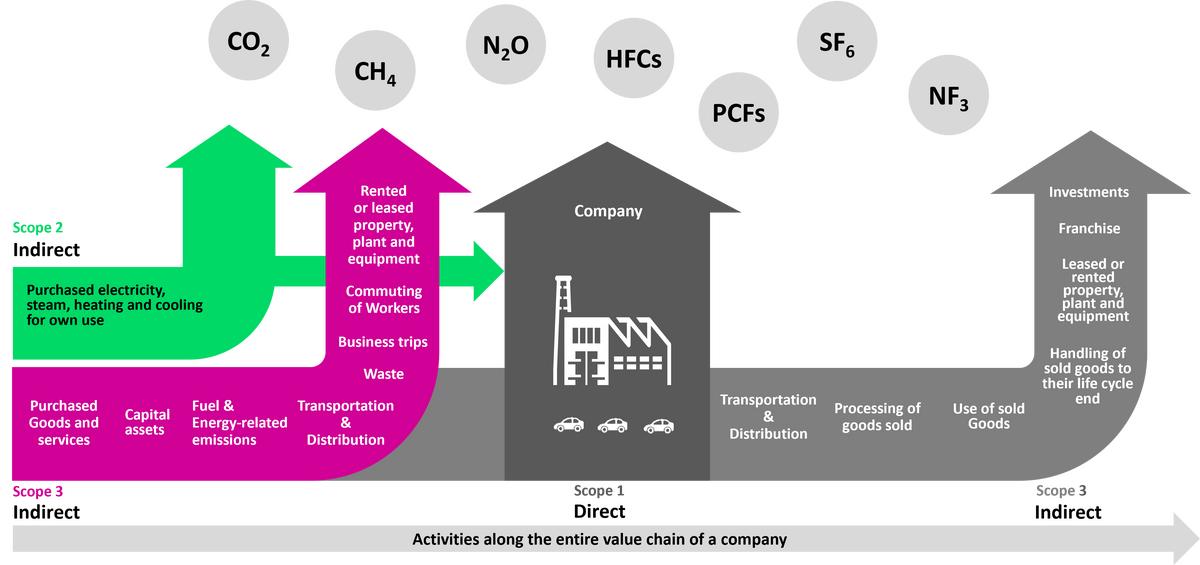

What does the Corporate Carbon Footprint include?

The Corporate Carbon Footprint (CCF) comprises the direct and indirect greenhouse gas emissions of the entire organisation.

Direct emitters include the company's own power plant or vehicle fleet, but also industrial processes such as cement or lime production.

Indirect emissions outside the company's boundaries include employee or customer travel, as well as transport and other activities.

The 3 scopes of the CCF

Scope 1: Emissions generated directly within the company, at a single location or part of the company (e.g. from the use of the company's own power plant or vehicle fleet)

Scope 2: Indirect emissions resulting from a company's energy consumption (e.g. electricity and heat consumption)

Scope 3: Indirect emissions along the value chain (business travel, manufacture of supplier products, transport, etc.)

When creating a CCF, systems that already collect environmental and energy data (e.g. ISO 14001 or ISO 50001, Emissions Trading or GRI standard) are helpful. The necessary structures for collecting climate-related data are therefore often already in place. For more information on the interrelationships, please take a look at our guide ‘From Energy to Climate Management’.

We are happy to combine our verification of your GHG balance with existing management systems or legal reporting requirements. Please feel free to ask us about this and take advantage of synergies.

In addition to specific greenhouse gas inventories, accounting tools and methodologies can also be tested and validated in accordance with the above-mentioned standards.

Any software solution that centralises and automates the collection and categorisation of greenhouse gas-related information and the calculation and accounting of greenhouse gases for reference values is a carbon footprint tool.

This includes, for example, Excel-based tools, browser-based applications or other individual software solutions.

Why have the CCF tool validated?

Normative requirements, internal organisational ideals and increasing customer demands are causing interest in greenhouse gas accounting to rise sharply – the market for carbon footprint tools is growing.

An external, independent review of your tool not only sets you apart from your competitors, but also strengthens its resilience and protects you against potential risks. Especially with newly developed methodologies, it is helpful to have their plausibility and functionality verified by an external review.

How does the validation of a CCF tool work?

An independent body compares calculation methods and (emission) data sources with the requirements of the relevant standard. For organisation-independent tools, the review can be carried out entirely through remote sessions and a desk review. Once any identified deficiencies have been demonstrably remedied, you will receive a confirmation of conformity for your tool.

In the subsidised transformation plans, companies should present and analyse their methodology for recording current greenhouse gas emissions (actual status) and a longer-term, concrete greenhouse gas target derived from this.

In order to embark on the path to carbon neutrality, the short-term and long-term decarbonisation strategies in the transformation plans should also be backed up with concrete measures and savings concepts.

What is eligible for government funding?

Funding is available to cover the costs incurred by any consulting organisations commissioned to prepare the balances and transformation plans and by auditing firms to verify the greenhouse gas balances.

Important: Scope 1 and 2 must be accounted for in order to receive government funding for your transformation plan. Accounting for Scope 3 is optional. However, for systematic climate protection management and to hedge your climate protection risks, a valid greenhouse gas balance sheet should always include indirect emissions from Scope 3.

We particularly like the interaction with the GUTcert auditors, who have a good understanding of the company-specific processes and procedures from many years of working together.

Michael Langenberg, REG Biofuels Germany GmbH

[Translated with DeepL]

The event was very informative and gave me many new ideas for improving our management. I should have taken this course much earlier in order to organise our system effectively. It gave us a very good understanding of the topic and enables me to better understand the auditors from the certification body. // Energiemanager ISO 50001

Sebastian Francke, Veolia Umweltservice PET Recycling GmbH

[Translated with DeepL]

Very interesting course with extensive considerations. The group work was very interesting and the dialogue with the participants was informative. The support and catering provided by the GUTcert team was once again excellent. Thank you very much! // Energiekennzahlen und Einflussfaktoren (ISO 50001 iVm ISO 50006, ISO 50015)

Thomas Hahn, Stadtwerke Lemgo GmbH

[Translated with DeepL]

I would never have thought that such a dry topic as a standard could be communicated so vividly, and with such a high degree of practical relevance. Well done! // ISO 9001:2015 - Qualitätsmanagementsysteme Lead Auditor (IRCA)

Clemens Rath, eBay International AG

[Translated with DeepL]

GUTCert is excellent at recognising the constantly changing reporting requirements, evaluating data systems and their plausibility, highlighting risks and making clear recommendations for action. GUTCert's consistent and very conscientious auditing has made a decisive contribution to avoiding compliance violations and the associated fines for Uniper.

Norman Thoms, Uniper

[Translated with DeepL]

We like the co-operation with GUTcert and the auditor very much. Our auditor communicates his findings with great expertise - the manner in which the audit is conducted is always pleasant and respectful.

Norbert Grabbe, Abbott Laboratories GmbH

[Translated with DeepL]

Our ISO 50001:2011 recertification audit was very well planned and conducted by the audit manager. He conducted the audit very competently, practically and purposefully. We are also very satisfied with the support provided by GUTcert GmbH.

Andrea Müller, Kirschneck GmbH Folienfabrik

[Translated with DeepL]

We have been CO2-neutral since 2010. Our environmental management system was the basis for this and has been certified since 1995.

Christoph Deinert, Märkisches Landbrot

[Translated with DeepL]

The training on audit techniques was very informative and helpful for practical work. You feel well prepared for the next audit! // Umweltbeauftragter / Auditor nach ISO 14001:2015

Heide Geber, Propapier PM1 GmbH

[Translated with DeepL]

Very interesting, informative event in which the extensive subject matter was presented in an entertaining way by the speaker. // Beauftragter für Integrierte Managementsysteme

Karin Ehrentraut, LUG aircargo handling GmbH

[Translated with DeepL]

Despite the extensive material, questions were answered in detail, which was very good. The available material is very comprehensive. // Umweltbeauftragter / Auditor nach ISO 14001:2015

Adrian Wieland, Gipscomm Energie

[Translated with DeepL]

The understanding of ISO 9001:2015 was conveyed with expertise and competence using practical scenarios! It was a pleasure to take part in the course! Thank you! // ISO 9001:2015 - Qualitätsmanagementsysteme Lead Auditor (IRCA)

Dirk Lewerenz, Bundesdruckerei GmbH

[Translated with DeepL]

In my opinion, this is a course that you should have attended before you start with quality management in the company. I can highly recommend this course. // Qualitätsbeauftragter ISO 9001:2015

The training was very exciting and realistic at all times. The knowledge imparted corresponds exactly to the daily requirements in my company, so this training was a great benefit for me. Thank you! // Energiebeauftragter / Energieauditor ISO 50001

Dieter Gawlick, John Deere GmbH & Co. KG

[Translated with DeepL]

The seminar was well prepared and the lecturer explained the topic very well. I personally took away a lot of information that will help me to introduce an occupational health and safety management system in my company. // Arbeitsschutzbeauftragter

Uwe Patscher, riha - Wesergold GmbH & Co. KG

[Translated with DeepL]

The quick and uncomplicated assessment of our system within the framework of the EEG since 2007, combined with the high level of commitment of the auditor, prompted us to also have the EnMS certified by GUTcert in 2013. We are very satisfied with the work carried out in both areas and are pleased with the expert contacts and friendly support.

Christina Henkel, Biogas Jena GmbH & Co. KG

[Translated with DeepL]

Comprehensive insight into ISO 9001, ISO 14001 and ISO 50001 as well as HLS. Practical examples were used to explain possibilities for integration into a comprehensive management system. Many practical tips for the design of future management systems! // Beauftragter für Integrierte Managementsysteme

Ulrich Stahl, En-Concept Energy Consultancy

[Translated with DeepL]

The lecturers are genuine experts who leave no questions unanswered. The course material is presented in a very clear and understandable way – highly recommended! // ISO/IEC 27001 Auditorenschulung gemäß IT-Sicherheitskatalog der Bundesnetzagentur

Kenji Tonio Kitamura

[Translated with DeepL]

It's nice to experience a wedding; information security meets the energy industry. // ISO/IEC 27001 Auditorenschulung gemäß IT-Sicherheitskatalog der Bundesnetzagentur

Marc Borgers, Informationssicherheitsberatung Marc Borgers

[Translated with DeepL]

The event provided a competent introduction to the implementation of AZAV and also made it possible to answer current and individual questions. // Qualitätsmanagement nach ISO 9001 für Bildungsträger

Arne Krüger, Samuel-Hahnemann-Schule

[Translated with DeepL]

A highly recommended course that provides a 360° view of all aspects of quality management for training organisations. The comprehensive topic was conveyed to the point. In addition, many important sources of information were mentioned as additional support. The course helps me a lot in my daily work. // Qualitätsmanagement nach ISO 9001 für Bildungsträger

Lisa Koglin

[Translated with DeepL]

GUTcert was a competent, fair and reliable partner at all times during the certification of our ISMS according to ISO 27001 and accompanied us with valuable tips and recommendations on the way from the pre-audit through Stage 1 to the successful certification audit.

Mario Konietzny, Stadtwerke Lutherstadt Eisleben GmbH

[Translated with DeepL]

Perfect event with very good framework conditions and first-class moderation by Mr Kroll. Interesting mix of speakers and topics.

Jörn Santore, Steinbeis Energie GmbH

[Translated with DeepL]

It was another very good and well-prepared event. I am going home with good ideas and suggestions. A lot of things are important for my work and help me in my daily tasks. I'll definitely be back! // GUTcert Neujahrstagung 2019

Thomas Hahn, Stadtwerke Lemgo GmbH

[Translated with DeepL]

Thank you very much for the interesting seminar, it was exactly what I was looking for! I learnt and consolidated many things and developed new ideas that will strengthen our operational sustainability. // Nachhaltigkeitsmanagement und -bericht in der Praxis

Dr. Nicole Diehlmann, Bechtle AG

[Translated with DeepL]

A very good theoretical introduction, usefully supplemented by practical exercises. // Nachhaltigkeitsmanagement und -bericht in der Praxis

Olaf Schlieper, Deutsche Zentrale für Tourismus

[Translated with DeepL]

As always very structured, with a lot of practical experience, therefore very helpful! // Nachhaltigkeitsmanagement und -bericht in der Praxis

Tobias Roesch, HC Starck GmbH Goslar

[Translated with DeepL]

The sustainability manager training programme gave me a very good grounding in my understanding of sustainable development. I am very pleased to have been shown new insights and approaches. // Nachhaltigkeitsmanagement und -bericht in der Praxis

Kristina Krüger, Stadtwerke Unna GmbH

[Translated with DeepL]

We have been completely satisfied with the cooperation from day one - fast, competent and customer-orientated at all times.

Jörn Seibert, AVU Serviceplus GmbH

[Translated with DeepL]

We have been receiving comprehensive and expert advice on the EEG, environmental assessments and interdisciplinary issues since 2009.

Thomas Fischer, Agrargenossenschaft Krippehna eG

[Translated with DeepL]

Thanks to GUTcert for the good handling as always!

A great refresher seminar with lots of practical examples and recommendations for practical action. The speaker impressed with his expertise, practical experience and professional competence. // Auffrischungskurs Energiemanagement: Aktuelles zu ISO 50000er-Reihe und Audits

Béla Gube, Philip Morris Manufacturing GmbH

[Translated with DeepL]

Very competent and understandable instructor. Pleasant training environment. I can only recommend it. // Energiebeauftragter / Energieauditor nach ISO 50001:2018

Aydin Kücük, FRONERI Schöller Produktions GmbH

[Translated with DeepL]

I have never experienced an external audit where it was completely clear from the outset that the focus was so clearly on potential for improvement and support for our organisation. That meant that the questions were no less critical and the discussions no less intense, but they were always goal-oriented. Everyone involved on our side saw the atmosphere and the benefits of the external audit in exactly the same way.

Dr. Walter Sucrow, Uniper Kraftwerke GmbH

[Translated with DeepL]

Relaxed, laid-back premises, great seminar with super lecturers and great food - five stars! // Qualitätsbeauftragter nach ISO 9001:2015

Thomas Schmidt, eCom Logistik GmbH

[Translated with DeepL]

In recent years, GUTcert's assessments have continued to improve, particularly in terms of transparency and clarity, and are – in contrast to other assessments – really good!

Dr. Martin Halwaß, C4 Energie AG

[Translated with DeepL]

High professionalism, customer-orientation and very good cooperation. I have known GUTcert for more than five years and all my experiences so far have always been very positive. A great achievement. Congratulations!

Camilo Gantiva, Francia Mozzarella GmbH

[Translated with DeepL]

We have been working successfully with GUTcert as a certification body for our ISO 50001 energy management system since 2018. The cooperation with GUTcert has been smooth and trusting so far. GUTcert has always responded to our needs and communication has been professional. The audit enabled us to identify and eliminate weaknesses and improve some of our energy management processes.

Steve Tobien, EDEKA Handelsgesellschaft Nord

[Translated with DeepL]

The audits with GUTcert have enabled us to optimise many areas of our work and thus sustainably develop our company.

Nadeshda Gudi, Ludwig Weinrich GmbH & Co. KG

[Translated with DeepL]

The audit was very pleasant, informative and very cooperative at a high level. We were able to communicate very well with the auditor and she was not sparing with constructive criticism. This is what we imagine an audit to be like! At the end of the day, this is helpful for everyone involved. The Globus management also shares this view.

Bernd Klemmer, Globus Gummiwerke GmbH

[Translated with DeepL]

Since 2016, the energy management system has ensured greater sustainability in our more than 450 branches and the administration of the Getränke Hoffmann Group. The creation of transparency and the significant reduction in energy costs are testimony to our sustainable company policy. In this way, we are doing our bit to combat global warming, which is very important to us!

Marcel Brauer, Getränke Hoffmann GmbH

[Translated with DeepL]

Our audit manager conducts each audit in a very practical manner, so that each audit results in added value for us.

Angelika Wittstock, RhönSprudel Gruppe

[Translated with DeepL]

We have been working successfully with our competence partner GUTcert since 2012. Since then, our energy management system has been continuously developed. A high level of transparency and evaluation of our systems allows us to eliminate weaknesses, recognise potential and consequently achieve our energy targets in the long term, which leads to the further development and increased efficiency of our company.

Matthias Karrenbauer, ROLAND MILLS UNITED GmbH & Co. KG

[Translated with DeepL]

When we have Prof Dr Lieback with us, it's always like a party - so refreshing and constructive: although it's an audit, we look forward to it because the auditors bring ideas with them - be it on the topics of quality management, occupational health and safety, hazardous substances or environmental protection.

Thomas Herfort, IMD Labor Oderland GmbH

[Translated with DeepL]

We are delighted with the expertise in AZAV provider certification and measure approval. The digitalised submission of evidence and documentation made it much easier for us to prepare for and follow up on the external audit. Thank you very much!

Elke Oertel, LeCA Jobtraining UG - vom BDSW zertifizierte Sicherheitsfachschule

[Translated with DeepL]

So far, we have only had good experiences of working in partnership with the team of auditors. The team at the certification body, with whom each company communicates in relation to project management, deadlines and documents, is also very personal and uncomplicated. We have the feeling that we are in good hands with GUTcert, that we are getting to know each other better and better and thus strengthening the good cooperation.

Nils Kuckert, Schornsteinfegerinnung

[Translated with DeepL]

Invers decided in favour of GUTcert for the auditing of DIN EN ISO 9001 and DIN ISO 45001 and we were completely convinced by the friendliness of the employees and the fast response time: We can recommend GUTcert without reservation.

The long period of cooperation since 1997/98 is proof enough of the valued and trusting collaboration. Anyone who voluntarily takes on EMAS and the ISO standards needs a reliable and practice-orientated certifier like GUTcert.

Bernhard Gillner, Aluminium Norf GmbH

[Translated with DeepL]

Through many years of testing the alternative system with GUTcert, we have learnt that communication is clear and no hidden costs are to be expected. These expectations were confirmed once again with the first ISO 9001 certification by GUTcert. In addition, we now benefit from a price advantage compared to previous years.

Thomas Jahn, OTEK Oberflächentechnik Kläke GmbH

[Translated with DeepL]

The course is a very good source of expertise for QMBs or people who want to carry out second or third party audits. // ISO 9001:2015 - Qualitätsmanagementsysteme Lead Auditor (IRCA)

Mario Mehrhoff, Hänsch GmbH

[Translated with DeepL]

The audit process with GUTcerts was very smooth, and the professionality of the auditor was outstanding. Our Auditor was very helpful with his insights and comments on our ISMS and I would like to forward to you our management’s appreciation for his excellent work.

Peter Mansour, IDEALworks GmbH

[Translated with DeepL]

We particularly liked the fact that the audit was not conducted exclusively as a question-and-answer catalogue, but rather as an interview with practical reference to the respective topic.

Michael Gültzow, Benway Solutions GmbH

[Translated with DeepL]

Our audit manager was well informed, the implementation was competent and always on time.

Achim Wetzel, IDR-Entsorgungsgesellschaft mbH

[Translated with DeepL]

There is an extremely trusting and very good business relationship between GUTcert and APM. As an auditor and expert, Mr Schruff is also available to answer questions outside the audits. Thank you very much for your support!

Everything was great! We are very satisfied with GUTcert and Mr Krause. We particularly liked the practical reference from other industries. In the case of Mr Krause, the glass industry.

Waldemar Meier, ADV - Augsburger Druck- und Verlagshaus GmbH

[Translated with DeepL]

What we particularly appreciate is the high level of expertise of our long-standing, reliable partner in terms of certification and verification. The audits are always very well structured and communicated. In addition, our audit manager is always setting priorities in order to optimise ongoing processes.

Thomas Kopenhagen, Aluminium Oxid Stade GmbH

[Translated with DeepL]

The cooperation is flawless and uncomplicated. We could be sure that nothing would be left undone and that the audit would be completed on time, even if changes/requests arose at short notice. We feel that we are in very good hands with GUTcert and look forward to working with them again.

Nigar Stücker, NaturStromTrading GmbH

[Translated with DeepL]

We would like to thank GUTcert for the optimal support in the certification process and for the always constructive and trusting cooperation.

Many thanks to the GUTcert audit team - you have guided us so wonderfully through this process, which has always given us confidence and courage!

Claudia Loewe, Deutsche Filmakademie Produktion GmbH

[Translated with DeepL]

The seminar completely fulfilled my expectations. The lecturers did a very good job of conveying the topic of calculating a corporate carbon footprint. The step-by-step instructions, exercises and practical examples were helpful, so that I can now apply the previously abstract topic in practice in my company. The structure of the seminar with different speakers was also very enjoyable, as the variety never got boring. The organisation (online seminar) also worked smoothly. Many thanks for two very informative days! // Klimamanagementbeauftragter (gn) im Unternehmen: Vom Corporate Carbon Footprint bis zur Klimaneutralität

Laura Holzer, WETgruppe – Wohnungseigentümer Gemeinnützige Wohnbaugesellschaft

[Translated with DeepL]

Thanks to the professional and thorough support from GUTcert, the plant registration in the register of guarantees of origin went smoothly and quickly. Any queries were dealt with comprehensively and promptly. We can highly recommend GUTcert as an expert and will be happy to work with them again in the future.

Andreas Ehrbar, aream GmbH

[Translated with DeepL]

The lecturer presented the contents of the standard and the audit techniques in a very understandable and practical manner. It was immediately apparent that he had in-depth specialist knowledge! Thank you very much for the enjoyable days, the lively discussions and the excellent catering. I would definitely recommend GUTcert. // Energiebeauftragter/-auditor nach ISO 50001

Christopher Witt, NORDFROST GmbH & Co. KG

[Translated with DeepL]

Even after our successful ISO 20121 certification, we continue to feel professionally and competently advised, always expertly accompanied on our ongoing path to sustainable event management. The advanced seminar provided us with an even more intensive insight and a profound understanding of the standard and its active implementation in our daily work processes.. // Beauftragter (gn) für Nachhaltiges Eventmanagement nach ISO 20121 – Aufbauseminar (Managementsystem)

Juliane Kranz, Deutsche Filmakademie Produktion GmbH

[Translated with DeepL]

Both the "Climate Management Officer" and "Environmental Management Officer" courses were of such a high quality that the realisation and implementation can be carried out very well in your own company afterwards. // Umweltbeauftragter nach ISO 14001:2015

Jan-Niklas Beicher, Fraunhofer Austria Research GmbH

[Translated with DeepL]

A very instructive and active training programme that I can wholeheartedly recommend to every (prospective) energy officer in a company. // Energiebeauftragter nach ISO 50001 (GUTcert)

Christian Schneider, Schattdecor SE

[Translated with DeepL]

In the years of cooperation, we have had various auditors in our company, but all of them were competent, honest, fair and you could immediately recognise that they were interested in advancing the company. The successful co-operation is already evident from the fact that Vosseler GmbH has been able to continuously improve and develop its management systems over the period of certification by GUTcert.

Martin-Werner Fazekas, Vosseler GmbH

[Translated with DeepL]

The e-learning is quite comprehensive and was a lot of fun for our sitemanagers as it is designed to be entertaining and practical. The films and questions in particular helped them to understand the subject matter.

As a result, the participants came up with a number of suggestions for savings and improvements. All in all, a very successful training course that I would be happy to recommend.// Energiemanagement nach ISO 50001:2018

Jochen Pöpken, Techem Energy Services GmbH

[Translated with DeepL]

We would particularly like to emphasise the good and professional service in the organisation of our ISO 14001 certification, which made the entire process run smoothly. In addition, the GUTcert Academy's training courses in environmental management are extremely helpful and have helped us to optimise our processes and make them more sustainable. Many thanks to the GUTcert team, we look forward to continuing our co-operation.

Jens Grossmann, RYGOL DÄMMSTOFFE GmbH & Co. KG

[Translated with DeepL]

Good, uncomplicated, friendly and fast service. A very good collaboration!

Kirsten Sonntag, Jung Papier GmbH

[Translated with DeepL]

Targeted seminar with an appropriate amount of information and competent teaching. // Klimamanagementbeauftragter (gn) im Unternehmen: Product Carbon Footprint (PCF) – Modul 2

Dr. Oliver Groß, BBIZ – Berliner Bildungs- und Integrationszentrum GmbH

[Translated with DeepL]

We would like to express our sincere thanks for the excellent cooperation in the context of our ISO 20121 certification. The GUTcert team was always available to us and impressed us with their high level of professionalism and humanity. We always felt we were in good hands and, looking back, we are convinced that we made absolutely the right choice. Thank you very much for your competent guidance and support on our way to sustainable event management.

David Baldig, George P. Johnson GmbH

[Translated with DeepL]

The lecturer had extensive practical and theoretical knowledge of the ISO 50001 standard, which he was able to convey competently and realistically. It was a very informative event, which I would highly recommend. // Energieauditor nach ISO 50001 (GUTcert)

Dirk Andersen, Georgsmarienhütte Holding GmbH

[Translated with DeepL]

From the very beginning, the GUTcert employees impressed us with their expertise, and the seminars they offered on ISO 20121 were a very important and valuable source of support. The list of costs was transparent and comprehensible, with no hidden surprises.

Isabella Anders, meplan GmbH

[Translated with DeepL]

Since 2023, GUTCert has been successfully auditing our quality and energy management in partnership with us and checking our environmental performance – reliably, quickly and smoothly. The findings identified in the audits always provide us with important input for the further development of our management system and the optimisation of our processes.

After switching to GUTcert, we couldn't be happier with our decision: all processes are fast, competent and extremely friendly. And thanks to the newsletter and the GUTcert Academy, we get everything we need – a perfect match for us!

Anne Augustin, QM-Beauftragte PLABIS Ingenieurgesellschaft mbH & Co.KG

[Translated with DeepL]

For our tank terminal, that is part of a leading company in sustainable fuels, the ISCC certificate is of great value if not indispensable. Thanks to the professional support and advice of GUT cert, we have held the ISCC certificate for many years already. We can recommend their support and services.

Kees de Jong, Neste Terminal Rotterdam

Great and educational event.

Thomas Dietrich, Zertifizierung Bau GmbH

[Translated with DeepL]

We are particularly impressed by the constructive cooperation with the office staff and the auditors on site during the certification process.

Jens Quandt, ReFood GmbH & Co.KG

[Translated with DeepL]

With the support of GUTcert, we have successfully recertified our QM system. Thank you very much for the excellent support and the smooth running of the recertification process!

Sebastian Stritz, QM-Beauftragter ITPower Solutions GmbH

[Translated with DeepL]

Working with GUTcert gives us the assurance that our commitment to sustainability is measurable and transparent.

Nelly Zeißig, Holtmann GmbH & Co.KG

[Translated with DeepL]

We thank GUTcert for their professional support during the certification process. Working with GUTcert helps us to further professionalise our working methods and efficiently advance our biomass projects at our facilities.

Dominik Wagner, C4 Energie GmbH

[Translated with DeepL]

GUTcert provides BioCirc with reliable support as an environmental verifier in the verification of our import consignments from Danish production for the German market. Their experienced and thorough inspection of non-German facilities, as well as their extensive team, gives us the necessary assurance.

Oliver Scharf, BioCirc

[Translated with DeepL]

We highly value the professional and solution-oriented collaboration with GUTcert. Their structured approach and clear communication significantly supported us in achieving and strengthening our management system.

Shota Kublashvili, FibreCoat GmbH

Ich habe das Seminar „Energiebeauftragter“ bei Ihnen besucht und war sowohl von den Inhalten als auch von der sehr professionellen Organisation und Durchführung überzeugt. Gerade die praxisnahe Aufbereitung der Themen und die klare Struktur des Seminars haben mir gezeigt, welchen Mehrwert Ihre Schulung für unser Unternehmen bietet. // Energiebeauftragter/-auditor (gn) nach ISO 50001

Thomas Bode, Sächsische Aufbaubank – Förderbank –

We are very satisfied with our collaboration with GutCert. The process, from placing the order to receiving the report, went smoothly and reliably. The team works professionally and efficiently, which makes things much easier for us as clients.

Farzad Mirdamadi, BEC – Energie Consult GmbH

[Translated with DeepL]

Die Trainerin hat die Unterrichtseinheiten hervorragend durchgeführt. Ihre Gabe, die Themen herauszubringen, das Praktische und die Theorie zusammen zu bringen geling ihr fantastisch.

Ich hoffe auf eine tolle Zusammenarbeit eines Tages. // Qualitätsmanagementsysteme Auditor / Lead Auditor (IRCA) nach ISO 9001:2015

Irina Höfer

Excellent service and a professionally conducted audit. From our point of view, the processes are optimal; there is currently nothing that needs improving.

Kai Minck, Orbia Polymer Solutions (Vestolit)

[Translated with DeepL]

Friendly, helpful and normally easy to get in touch.

Mounir El’Mourabit, Vartdal Plastindustri AS

Der Emissionshandel-Betriebsbeauftragte in der 4. Handelsperiode mehr Infos